1. What is the FPGA Security Market Overview – definition, scope, and significance?

The FPGA Security Market encompasses hardware‑based security solutions that leverage Field‑Programmable Gate Arrays (FPGAs) to protect data, intellectual property, and system integrity across diverse applications. It includes secure boot, encryption, tamper detection, and authentication functions implemented on reconfigurable silicon. The market’s scope covers end‑user segments such as telecommunications, consumer electronics, data centers, military & aerospace, industrial, automotive, and other niche domains, as well as technology families (SRAM, Flash, Antifuse) and configuration classes (low‑end, mid‑range, high‑end). Its significance stems from the growing need for on‑chip, low‑latency security in a world of increasingly sophisticated cyber threats, where traditional software‑only approaches are insufficient.

2. What are the key drivers, restraints, challenges, and opportunities in the FPGA Security Market?

Primary drivers include rising cyber‑attack frequency, demand for secure 5G infrastructure, and the migration of workloads to edge and cloud data centers that require hardware‑rooted protection. Regulatory pressures for secure communications in military and aerospace also boost adoption. Restraints involve the higher cost of high‑end FPGAs compared with ASIC alternatives and a shortage of skilled engineers proficient in hardware security design. Challenges revolve around ensuring rapid time‑to‑market while maintaining rigorous validation standards. Opportunities arise from emerging IoT ecosystems, the expansion of autonomous vehicle platforms, and the development of post‑quantum cryptographic primitives that can be instantiated on reconfigurable fabrics.

3. What growth trends are currently shaping the FPGA Security Market?

Current trends feature the integration of security IP cores directly into FPGA design flows, enabling designers to embed encryption, secure key storage, and side‑channel countermeasures early in development. Another trend is the convergence of AI accelerators with security functions, allowing on‑the‑fly protection of inference workloads. Additionally, cloud service providers are offering FPGA‑as‑a‑service (FaaS) with built‑in security enclaves, driving broader adoption among developers who lack in‑house hardware expertise.

4. How has COVID‑19 impacted the FPGA Security Market and what is the recovery trajectory?

The pandemic initially disrupted supply chains for semiconductor fabs, causing a temporary slowdown in FPGA shipments. However, the rapid shift to remote work and the acceleration of digital transformation heightened demand for secure communication and cloud‑based processing, offsetting early losses. Post‑2022, the market has entered a strong recovery phase, reflected in robust growth expectations and a rebound in R&D spending for security‑focused FPGA solutions.

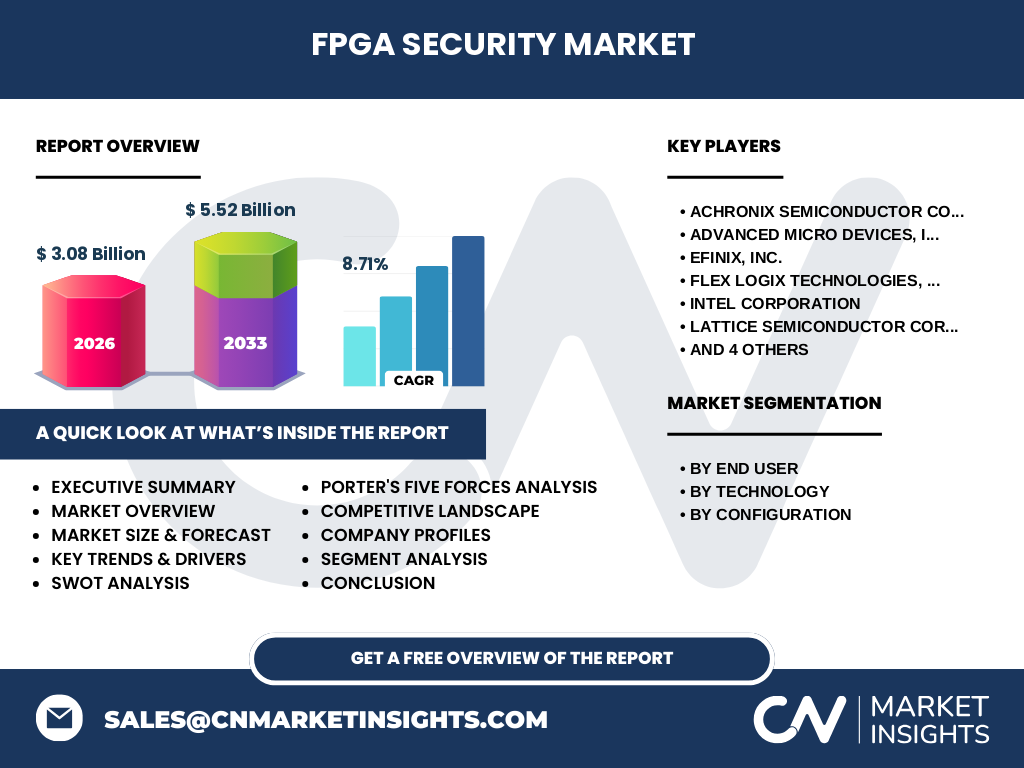

5. Who are the major competitors and what is the current state of market consolidation?

Key competitors include Achronix Semiconductor Corporation, Advanced Micro Devices, Inc., Efinix, Inc., Flex Logix Technologies, Inc., Intel Corporation, Lattice Semiconductor Corporation, LeafLabs, LLC, Microchip Technology Inc., QuickLogic Corporation, and S2C. The competitive landscape is marked by strategic partnerships and acquisitions aimed at expanding security IP portfolios, but overall consolidation remains moderate, with each player maintaining distinct technology differentiators—such as low‑power SRAM cores, high‑performance Flash‑based devices, or antifuse‑based secure modules.

6. What are the high‑level findings of the Executive Summary?

The FPGA Security Market is projected to reach US$3.08 billion in 2026 and grow to US$5.52 billion by 2033, delivering a compound annual growth rate (CAGR) of 8.71 %. Growth is driven by heightened security requirements across telecom, data center, and defense sectors, as well as by the emergence of secure edge computing. While cost sensitivity and talent gaps pose challenges, the market offers significant upside through innovation in post‑quantum cryptography and integrated security‑AI accelerators.

7. What are the forecast expectations for the FPGA Security Market from 2025 to 2032?

Building on the 2026 base of US$3.08 billion, the market is expected to expand to approximately US$5.52 billion by 2033, reflecting an 8.71 % CAGR. This trajectory suggests a steady increase in annual revenues, underpinned by continued adoption in high‑growth segments such as data centers, 5G backhaul, and autonomous vehicles. Forecasts anticipate a gradual shift toward mid‑range and high‑end FPGA configurations as security demands become more complex.

8. How is the market sized and shared by end‑user, technology, and configuration segments?

Segment analysis reveals that telecommunications and data centers dominate usage, leveraging high‑performance FPGA security for network encryption and secure compute. Consumer electronics and automotive follow, employing low‑to‑mid‑range devices for secure boot and OTA updates. Technology‑wise, SRAM‑based FPGAs capture the largest share due to their reconfigurability and lower power, while Flash and Antifuse serve niche high‑risk domains that require non‑volatile or one‑time programmable security. Configuration segmentation shows a balanced distribution: low‑end FPGAs address cost‑sensitive IoT devices, mid‑range solutions serve most telecom and industrial use cases, and high‑end FPGAs are reserved for defense, aerospace, and high‑throughput data‑center workloads.

9. What is the global market size and share by region?

Although precise regional dollar values are not disclosed, the market’s geographic spread aligns with major technology hubs. North America leads in enterprise and defense adoption, Europe follows with strong automotive and industrial demand, and the Asia‑Pacific region shows the fastest growth driven by telecom rollout and manufacturing of consumer electronics. The rest of the world contributes a modest but steady share, reflecting expanding security awareness in emerging economies.

10. How does each region perform in the FPGA Security Market?

North America benefits from a mature ecosystem of cloud providers, defense contractors, and R&D centers, resulting in high per‑capita spend on secure FPGA solutions. Europe’s performance is bolstered by stringent data‑privacy regulations and a thriving automotive sector, prompting investments in secure boot and secure communication. Asia‑Pacific exhibits rapid expansion due to 5G deployments, large‑scale consumer device manufacturing, and government‑backed initiatives for secure IoT infrastructure. The Middle East & Africa and Latin America represent emerging opportunities, with early pilots in secure communications and industrial automation.

11. Which companies lead the FPGA Security Market and what are their strategies?

Intel Corporation leads with its Stratix and Arria families, emphasizing integrated security IP and cloud‑service partnerships. AMD leverages its acquisition of Xilinx to combine high‑performance compute with robust encryption engines. Achronix focuses on high‑bandwidth memory interfaces for data‑center security. Lattice differentiates through low‑power, cost‑effective SRAM devices for edge IoT. Efinix and Flex Logix target rapid time‑to‑market with modular security cores. Microchip and QuickLogic pursue automotive and industrial segments by embedding secure boot and key‑management blocks directly into their FPGA lines. These strategies reflect a mix of portfolio breadth, application‑specific targeting, and ecosystem collaboration.

12. What does Porter’s Five Forces reveal about the FPGA Security Market?

Threat of New Entrants: Moderate – high development costs and IP barriers limit newcomers, yet emerging fabless startups can exploit niche security IP. Bargaining Power of Suppliers: Low to moderate – semiconductor fabs are limited but multiple foundries mitigate supplier leverage. Bargaining Power of Buyers: Growing – large cloud providers and defense agencies demand customized security solutions, increasing their negotiating strength. Threat of Substitutes: Low – software‑only security lacks the hardware root‑of‑trust that FPGAs provide, keeping substitution risk limited. Industry Rivalry: Intense – leading vendors vie for market share through IP integration, pricing, and strategic alliances.

13. What are the SWOT highlights for the FPGA Security Market?

Strengths: Reconfigurability, low latency, hardware root‑of‑trust, and strong IP ecosystems. Weaknesses: Higher unit cost versus ASICs, limited design‑skill pool, and longer validation cycles. Opportunities: Post‑quantum cryptography implementation, secure AI acceleration, and expansion into automotive‑grade safety‑critical systems. Threats: Rapid evolution of cyber‑attack techniques, supply‑chain disruptions, and potential regulation that could favor open‑source security solutions.

14. How is value created and transferred in the FPGA Security Market value chain?

The value chain begins with semiconductor fabs producing raw FPGA silicon, followed by IP vendors supplying security cores (encryption, key management, tamper detection). FPGA manufacturers integrate these IPs, add design tools, and deliver development kits. System integrators then embed secure FPGAs into end‑product designs, while software developers provide firmware and validation suites. Finally, distributors and cloud service providers deliver the finished secure solutions to end users, completing the loop with after‑sales support and firmware updates.

15. What investment insights should stakeholders consider?

Investors should focus on companies that own both silicon and security IP, as they can capture higher margins and accelerate time‑to‑market. Funding R&D in post‑quantum and AI‑enabled security will likely yield differentiated products. Partnerships with cloud platform providers and defense contractors can secure long‑term contracts. Conversely, be cautious of firms overly reliant on low‑margin, low‑end FPGA segments without a clear security roadmap.

16. What are the concluding takeaways from the FPGA Security Market analysis?

The FPGA Security Market is on a clear growth path, underpinned by a 8.71 % CAGR and a projected market size of US$5.52 billion by 2033. Security concerns across telecom, data centers, and defense drive demand for hardware‑rooted protection. While cost and talent gaps pose challenges, the market offers compelling opportunities through innovative security IP, emerging applications, and strategic collaborations. Stakeholders who invest in integrated security solutions and address talent shortages are positioned to capture the most value.

17. How was the research conducted for this report?

The study combined primary interviews with industry experts, secondary data from company filings, market intelligence databases, and published research on semiconductor security trends. Quantitative modeling used the provided base year (2026) size of US$3.08 billion and applied the stated CAGR of 8.71 % to forecast the 2033 market value. Qualitative insights were derived from technology roadmaps, regulatory analysis, and competitive positioning of the listed key companies.

18. What is the scope of this research?

The scope covers global FPGA security solutions across all major end‑user verticals, technology families (SRAM, Flash, Antifuse), and configuration tiers (low‑end, mid‑range, high‑end). Geographic coverage includes North America, Europe, Asia‑Pacific, and emerging markets. The analysis excludes unrelated FPGA applications such as general‑purpose compute that do not incorporate dedicated security functions.

19. Which key companies have recent developments in the FPGA Security Market?

Intel announced a new secure‑boot IP block for its Agilex series, targeting 5G base stations. AMD’s Xilinx division released a post‑quantum encryption core for its Versal AI Core devices. Achronix introduced a high‑throughput TLS accelerator for data‑center cards. Lattice launched a low‑power, automotive‑qualified SRAM FPGA with built‑in tamper detection. Flex Logix partnered with a leading cloud provider to offer FPGA‑as‑a‑service with encrypted execution environments. These developments illustrate a market moving rapidly toward integrated, application‑specific security solutions.